Penalty for not registering GST in India can expose businesses to financial fines, interest liability, and legal enforcement under GST law. Ignoring GST registration requirements in India can expose businesses to financial penalties, interest liability, tax recovery proceedings, and even prosecution under the Goods and Services Tax framework. Many small businesses, freelancers, and online sellers unknowingly operate without GST registration due to confusion about turnover thresholds or compulsory registration rules, only to receive compliance notices later from tax authorities.

Penalty for not registering GST in India refers to statutory fines, interest liability, and enforcement actions imposed when businesses fail to obtain GST registration despite eligibility.

This comprehensive guide explains the penalty for not registering GST in India, covering legal provisions, penalty calculation, interest implications, officer verification workflow, real risk scenarios, and practical strategies to prevent compliance trouble. Whether you are a trader, service provider, online seller, or startup founder, understanding these consequences is essential to protect your business from financial and legal risks.

Under Section 122 of the CGST Act, failure to obtain GST registration when legally required attracts a penalty of ₹10,000 or the tax amount due, whichever is higher, along with interest liability under Section 50 and potential recovery proceedings initiated by GST authorities.

Key Rule:

GST registration is mandatory once eligibility criteria are met, and failure to register triggers penalty, interest, and enforcement proceedings.

Before evaluating penalties, businesses should confirm whether GST registration was mandatory by reviewing GST turnover limit in India for registration.

If your business qualifies for GST, you should immediately follow the step-by-step process to apply for GST registration online in India to avoid compliance notices and penalties.

To understand the broader legal framework, review the complete GST registration in India guide covering eligibility, documents, fees, and timeline before evaluating penalty implications.

| Key Question | Quick Answer |

|---|---|

| Is GST registration mandatory? | Yes once eligibility arises under CGST Act |

| Penalty for not registering GST? | ₹10,000 or tax amount due (whichever higher) |

| Can GST department detect non-registration? | Yes via data analytics, AIS, vendor mismatch |

| Can late registration remove penalty? | No, but may reduce enforcement severity |

| Safest strategy? | Register immediately after eligibility |

What Happens If You Do Not Register for GST in India?

Non-registration under GST when legally required can trigger multiple enforcement actions by tax authorities, including penalty imposition, interest liability, tax recovery proceedings, and scrutiny of business transactions. Beyond monetary consequences, non-compliance may impact vendor relationships, input tax credit eligibility, and financial credibility.

- Monetary penalties under GST law

- Interest on unpaid tax liability

- Tax recovery proceedings and notices

- Loss of input tax credit eligibility

- Vendor and marketplace compliance issues

- Higher audit and verification risk

- Possible prosecution in deliberate cases

GST non-registration is not merely a procedural lapse — it creates cumulative financial and compliance risk for businesses.

— LocalGrow Digital

Is GST Registration Mandatory for All Businesses in India?

GST registration is mandatory only when businesses cross prescribed turnover thresholds or fall under compulsory registration categories such as interstate supply, online marketplace selling, export of services, or taxable service provision. However, misunderstanding eligibility rules remains a major reason businesses receive penalty notices.

Online marketplace sellers should review GST for online sellers in India mandatory registration rules because compulsory registration applies regardless of turnover in many cases.

Registered Business Advantages

- Input tax credit eligibility

- Vendor compliance acceptance

- Marketplace selling approval

- Financial credibility

- Legal protection

Non-Registered Business Risks

- Monetary penalties

- Interest liability

- Compliance notices

- Vendor restrictions

- Audit risk

Table of Contents

How Much Penalty Is Charged for Not Registering GST in India? Complete Calculation Guide

What Is the Minimum Penalty for Not Registering GST in India?

Failure to obtain GST registration when legally required attracts statutory penalties under the CGST Act. Many businesses assume non-registration only delays compliance, but authorities treat it as a tax violation that can lead to penalty imposition, interest liability, and recovery proceedings depending on the scale and duration of non-compliance.

The penalty framework varies based on tax liability, turnover during non-registration period, and whether the lapse is considered procedural or intentional. Understanding how GST penalties are calculated helps businesses assess financial exposure and take corrective action before enforcement escalates.

| Scenario | Penalty Amount | Legal Reference | Risk Level |

|---|---|---|---|

| Non-registration when required | ₹10,000 or tax amount due (higher) | Section 122 CGST | Medium |

| Intentional tax evasion | 100% of tax due | Section 122 & 74 | High |

| Delay causing tax loss | Interest + penalty | Section 50 | Medium |

| Fraudulent activity | Prosecution possible | Section 132 | Very High |

GST penalty is calculated not only on procedural lapse but also on tax revenue risk perceived by authorities.

— LocalGrow Digital

How Do GST Authorities Calculate Penalty for Non-Registration?

GST authorities calculate penalty by assessing the tax that should have been paid during the period of non-registration. This retrospective assessment involves evaluating turnover, determining applicable GST liability, applying interest on unpaid tax, and imposing statutory penalty under relevant CGST provisions.

Businesses often underestimate cumulative exposure because penalty is only one component — interest and tax recovery significantly increase financial liability.

- Determine turnover during non-registration period

- Calculate tax liability retrospectively

- Apply interest under Section 50

- Impose penalty under Section 122

- Initiate recovery if unpaid

GST Non-Registration Penalty Definition:

Penalty applies when a business fails to obtain GST registration despite eligibility, resulting in retrospective tax liability, interest, and enforcement proceedings.

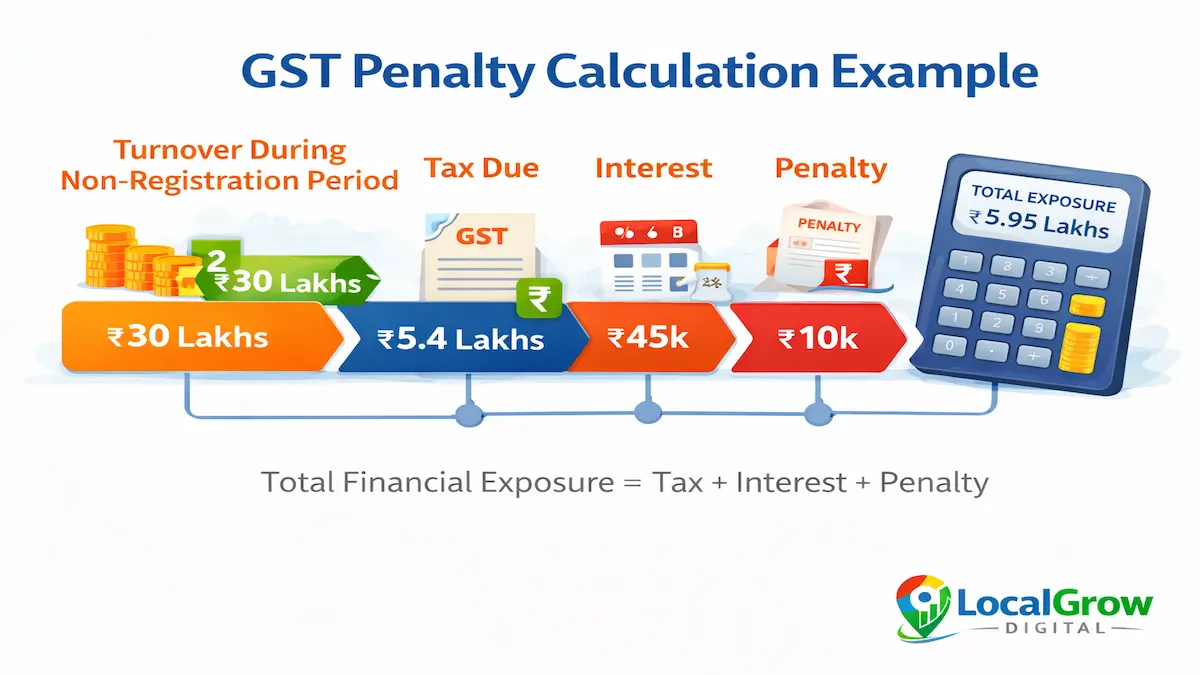

| Turnover | Tax Due | Interest (approx) | Penalty | Total Exposure |

|---|---|---|---|---|

| ₹15L | ₹2.7L | ₹20k | ₹10k | ₹3L+ |

| ₹30L | ₹5.4L | ₹45k | ₹10k | ₹5.9L+ |

| ₹50L | ₹9L | ₹90k | ₹10k | ₹10L+ |

Many businesses underestimate cumulative penalty exposure until calculation is performed. Seeking expert guidance early helps prevent incorrect estimation and delayed compliance action.

How Much Interest Is Charged for Late GST Registration in India?

Interest liability applies when tax remains unpaid during the period a business operated without GST registration. Under Section 50 of the CGST Act, interest is calculated from the date tax became payable until the date of actual payment after registration.

This means that even if penalty is minimal, interest continues accumulating daily, significantly increasing total compliance cost for businesses delaying GST registration.

- Interest rate typically 18% per annum

- Calculated daily on unpaid tax

- Applies even if penalty is waived

- Continues until tax payment completion

Low Risk Case

- Voluntary late registration

- Short delay

- No tax evasion intent

High Risk Case

- Long non-registration period

- Significant turnover

- Intentional non-compliance

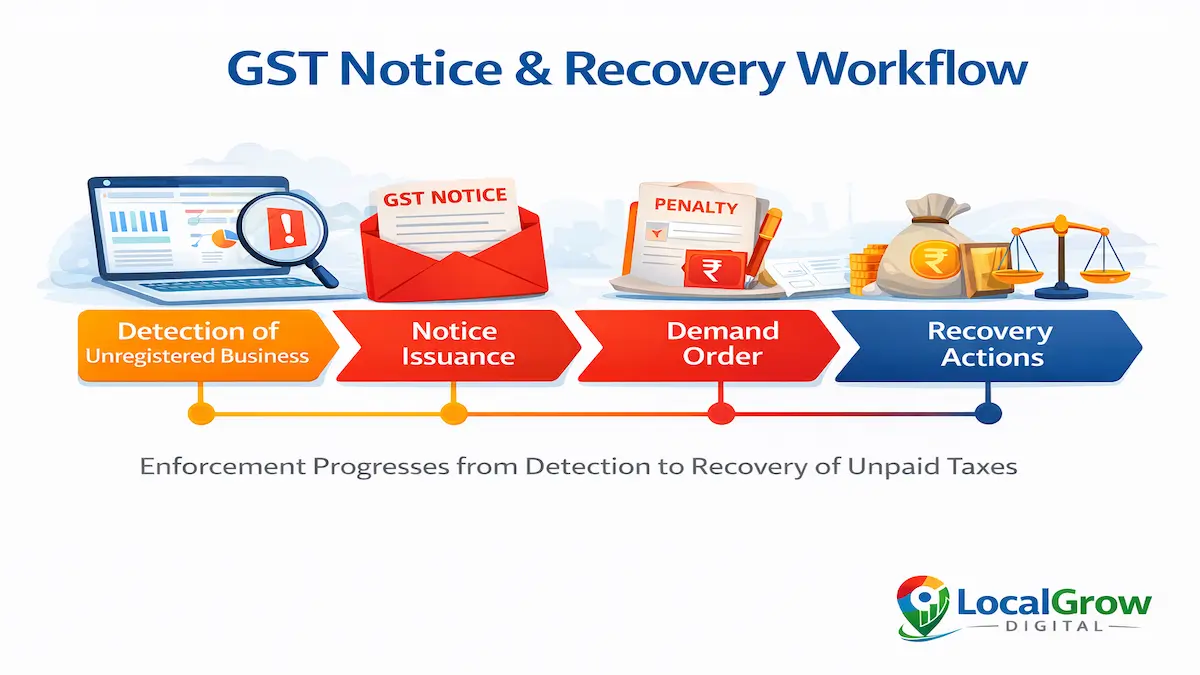

What Happens When GST Authorities Detect Unregistered Business Activity?

When GST authorities detect taxable activity conducted without registration, they initiate enforcement procedures that may include notices, tax demand orders, and recovery proceedings. Detection often occurs through vendor mismatch data, marketplace reporting, bank transaction analysis, or analytics-based compliance monitoring.

The recovery process aims to recover unpaid tax, interest, and penalties while ensuring future compliance through mandatory registration enforcement.

- Detection via data analytics or vendor mismatch

- Notice issuance for registration and tax payment

- Demand order with tax and penalty

- Recovery proceedings if unpaid

- Possible bank attachment or property recovery

GST enforcement has become increasingly data-driven, making non-registration easier for authorities to detect.

— LocalGrow Digital

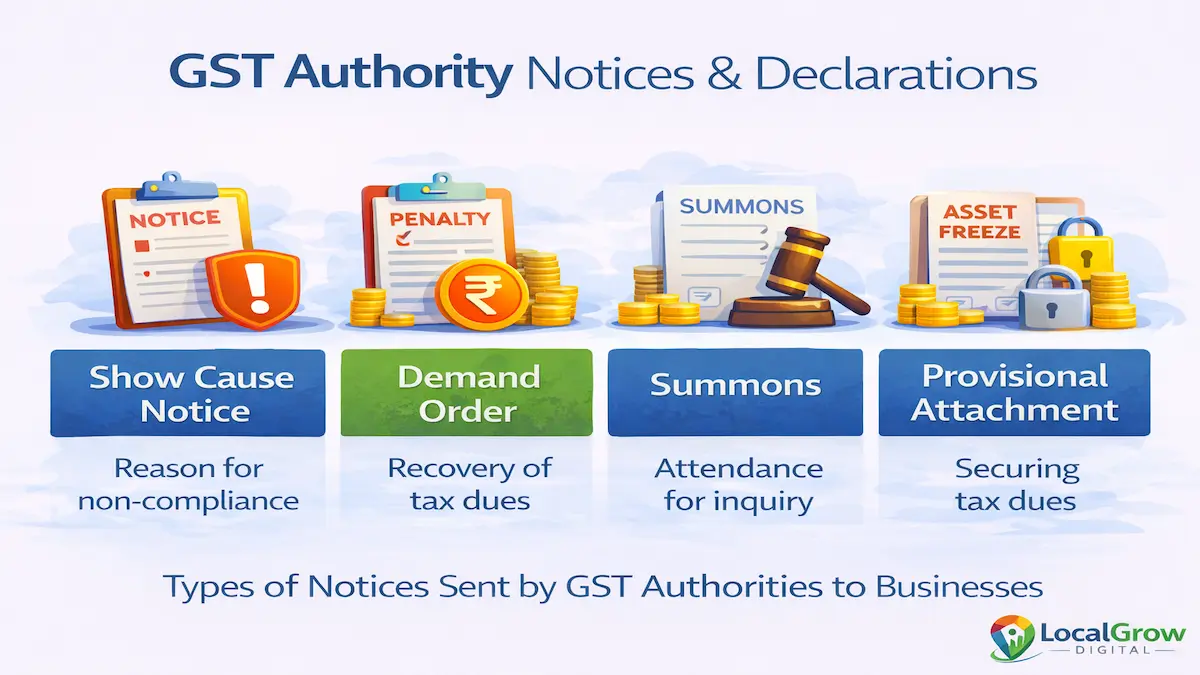

What Notices Can GST Officers Issue for Non-Registration? Full Lifecycle Explained

GST officers follow a structured notice lifecycle when dealing with unregistered taxable activity. Understanding this lifecycle helps businesses anticipate enforcement actions and respond promptly to minimize penalty exposure.

These notices may range from registration directives and clarification requests to demand orders and recovery proceedings depending on severity of non-compliance.

- Detection of taxable activity

- Notice for explanation or registration

- Assessment of tax liability

- Demand order issuance

- Penalty imposition

- Recovery proceedings

| Scenario | Officer Action | Business Impact |

|---|---|---|

| Short delay | Notice + penalty | Low |

| Moderate delay | Demand order | Medium |

| Long delay | Recovery action | High |

| Intentional evasion | Prosecution risk | Very High |

Businesses receiving notices during late registration should understand GST registration rejected in India corrective strategies to avoid repeated compliance complications.

Late registration may also increase cost exposure, so businesses should review GST registration fees in India government vs professional cost breakdown before initiating compliance.

Can GST Department Detect Unregistered Businesses in India?

GST Detection Rule:

Authorities detect unregistered businesses through data analytics, marketplace reporting, banking transactions, and vendor mismatch signals.

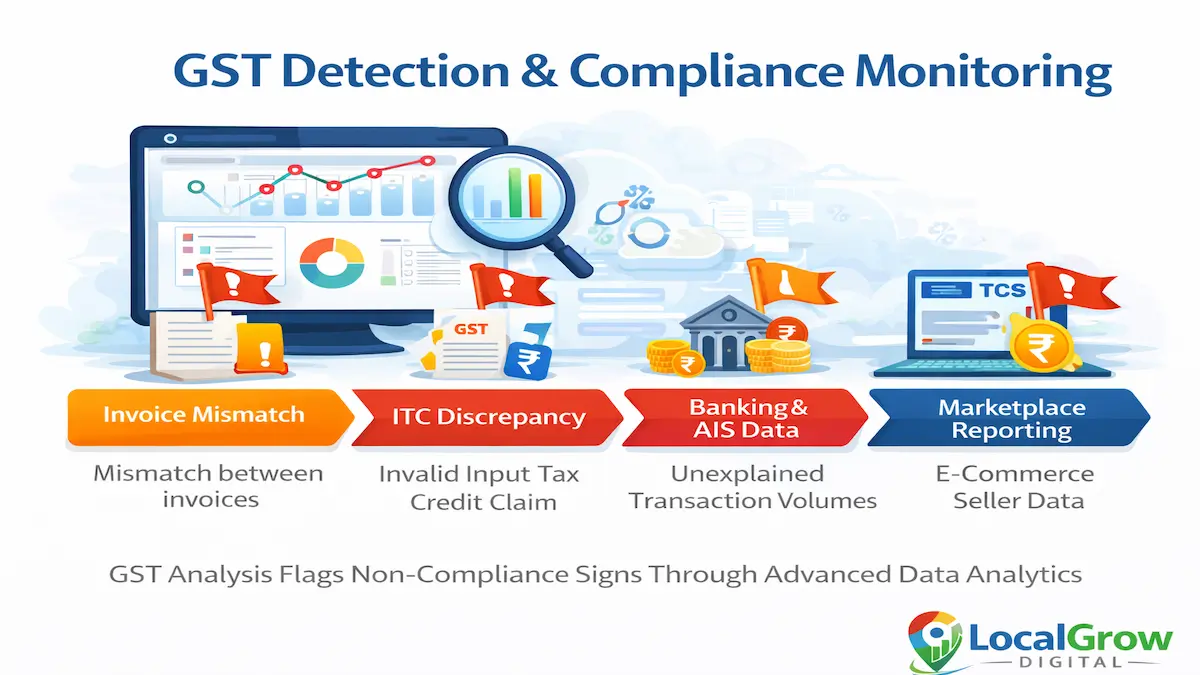

Yes — GST authorities increasingly detect unregistered businesses through advanced data analytics, marketplace reporting, banking transaction trails, and vendor compliance mismatch analysis. The GST ecosystem is highly interconnected, meaning a business operating without registration often leaves digital footprints that trigger compliance alerts even without physical inspection.

Many small businesses assume that operating without GST registration remains unnoticed until they voluntarily apply, but authorities now leverage automated risk detection systems integrating GSTR filings, e-commerce TCS data, AIS financial information, and vendor purchase records. This makes detection probability significantly higher compared to earlier tax regimes.

- Vendor purchase mismatch detection

- Marketplace TCS reporting (Amazon, Flipkart, Meesho)

- Bank transaction analytics and AIS data

- GSTR reconciliation mismatch

- Input tax credit claims by vendors

- E-invoice and e-way bill trail

- Data analytics based compliance monitoring

If your business generates digital transaction trails, proactive registration significantly reduces risk of automated detection and enforcement action.

GST detection today is largely data-driven, making non-registration difficult to sustain in digitally connected business ecosystems.

— LocalGrow Digital

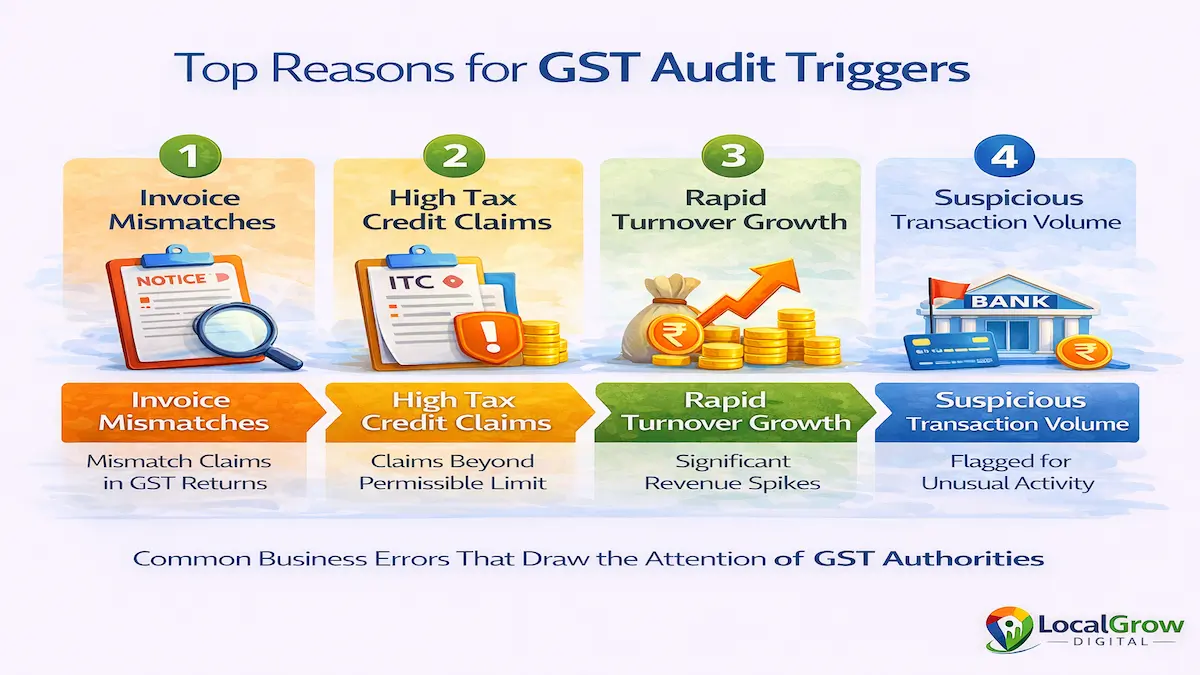

How Do GST Authorities Identify Unregistered Taxable Activity?

GST authorities identify unregistered businesses through cross-verification of transactional data across multiple sources. When a registered vendor reports sales to a buyer lacking GST registration, automated mismatch signals may trigger scrutiny. Similarly, financial intelligence systems monitor bank transaction volumes inconsistent with declared tax registrations.

E-commerce platforms play a major role in detection because they report seller transaction data through TCS mechanisms. This means online sellers operating without GST registration can be flagged even when turnover appears below threshold limits due to compulsory registration rules.

| Detection Source | Authority Interpretation | Risk Level |

|---|---|---|

| Vendor purchase mismatch | Hidden taxable activity | Medium |

| Marketplace TCS data | Interstate taxable supply | High |

| AIS financial data | Undeclared turnover | Medium |

| E-way bill trail | Goods movement evidence | High |

| Bank transaction analytics | Business activity indication | Medium |

What Business Types Face Higher Risk of GST Detection Without Registration?

Certain business models face elevated detection risk because their operations generate digital compliance trails. Understanding these scenarios helps businesses assess exposure and take preventive action before receiving notices.

- Online marketplace sellers

- Interstate suppliers

- Service exporters

- Freelancers with foreign clients

- Dropshipping businesses

- High-volume digital service providers

- Traders issuing invoices without GST

Freelancers providing interstate or export services should review GST for freelancers and service providers in India compliance rules to evaluate registration requirements and avoid penalty exposure.

Can Freelancers and Small Businesses Get GST Penalty Without Registration?

Yes — freelancers and small businesses can face GST penalties if they fall under compulsory registration categories or exceed turnover thresholds. Many freelancers mistakenly assume small scale operations remain exempt, but interstate service provision and export of services often trigger mandatory registration requirements regardless of turnover.

Authorities evaluate transaction patterns, client location, and banking data to determine whether freelancers should have registered earlier. Failure to do so may result in retrospective tax liability and penalty assessment.

Low Detection Risk Scenario

- Local services below threshold

- No interstate supply

- Minimal digital trail

High Detection Risk Scenario

- Marketplace selling

- Export services

- Interstate transactions

- Vendor mismatch records

Does Selling on Amazon or Flipkart Without GST Increase Penalty Risk?

Yes — selling on e-commerce platforms without GST registration significantly increases detection probability due to compulsory registration provisions and transaction reporting requirements. Marketplaces collect TCS and share seller data with GST authorities, creating a transparent compliance trail.

Online sellers should understand compliance rules explained in sell without GST on Amazon Flipkart Meesho legal implications guide before continuing operations without registration.

E-commerce compliance integration makes marketplace sellers among the most easily detectable unregistered businesses.

— LocalGrow Digital

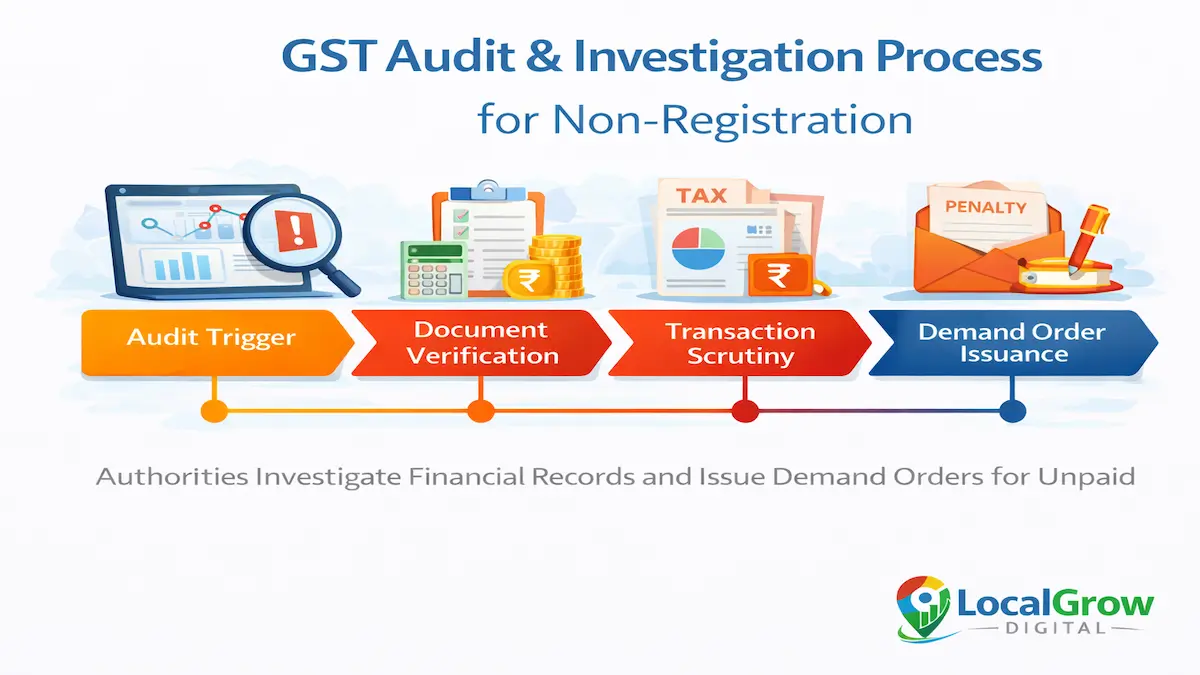

Can GST Department Conduct Audit or Investigation for Non-Registration?

GST authorities may initiate audit or investigation when data analytics indicate potential non-registration despite taxable activity. Such investigations may involve document verification, transaction analysis, bank record scrutiny, and demand orders for retrospective tax liability.

Audit risk increases when vendors claim input tax credit against purchases from unregistered entities, triggering automated mismatch alerts that prompt departmental scrutiny.

| Investigation Trigger | Authority Action | Business Impact |

|---|---|---|

| Vendor ITC mismatch | Notice issuance | Medium |

| Marketplace data mismatch | Registration demand | High |

| AIS income mismatch | Financial scrutiny | Medium |

| E-way bill mismatch | Goods movement verification | High |

Are Penalties Higher for Compulsory GST Registration Categories?

Yes — penalties may become more severe when businesses fall under compulsory registration categories yet continue operations without GST compliance. Compulsory registration applies regardless of turnover in cases such as interstate supply, e-commerce selling, export of services, and reverse charge scenarios. Authorities treat violations in these categories with greater scrutiny because tax leakage risk is inherently higher.

Businesses often misunderstand exemption thresholds and assume turnover-based relief applies universally. However, compulsory registration provisions override turnover limits, making non-registration a statutory violation even at lower turnover levels.

| Category | Registration Rule | Penalty Exposure | Risk Level |

|---|---|---|---|

| Interstate supply | Mandatory | Tax + penalty | High |

| E-commerce sellers | Mandatory | Penalty + ITC loss | High |

| Export services | Mandatory | Interest + penalty | Medium |

| Reverse charge cases | Mandatory | Recovery proceedings | Medium |

Does Interstate Supply Without GST Registration Increase Penalty Risk?

Yes — interstate supply triggers compulsory GST registration irrespective of turnover. Businesses supplying goods or services across state borders without registration may face retrospective tax liability, penalty imposition, and interest charges once authorities detect cross-state transactions.

Detection often occurs through e-way bill data, vendor compliance mismatch, or marketplace transaction records showing interstate supply patterns. Businesses operating remotely or serving clients across states must carefully evaluate registration obligations.

Is Selling Online Without GST Considered a Serious Compliance Violation?

Selling through e-commerce marketplaces without GST registration is considered a significant compliance risk because marketplaces report seller transaction data to GST authorities via TCS mechanisms. This creates a transparent digital trail enabling authorities to identify non-registered sellers even when turnover appears modest.

Online sellers should carefully review compliance implications explained in GST for online sellers in India mandatory rules to avoid penalty exposure.

Marketplace integration has transformed GST compliance from voluntary discipline into data-verified enforcement.

— LocalGrow Digital

Can Exporters and Freelancers Face GST Penalty Without Registration?

Yes — exporters and freelancers providing services to international clients often fall under compulsory registration provisions despite low turnover because export transactions require GST compliance for zero-rated supply benefits. Non-registration may lead to penalty, interest liability, and denial of export-related tax benefits.

Freelancers should verify eligibility rules discussed in GST for freelancers and service providers in India compliance guide before continuing operations without registration.

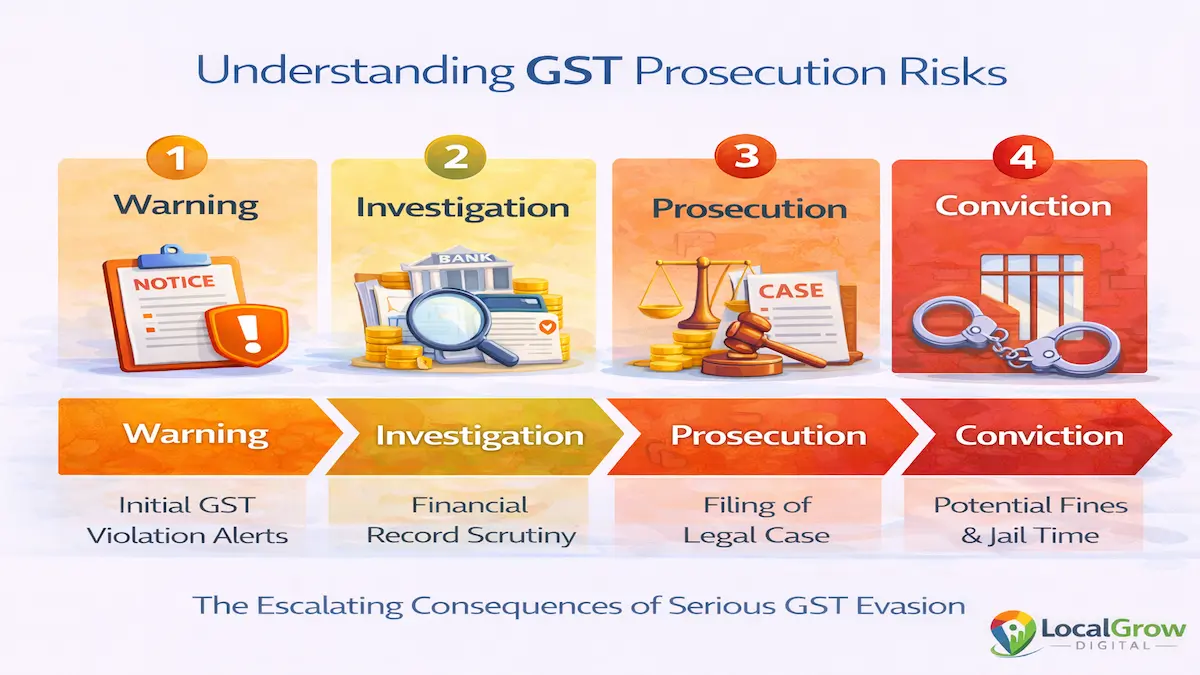

Can GST Non-Registration Lead to Prosecution or Legal Action?

Yes — severe non-registration cases involving tax evasion, deliberate suppression of turnover, or fraudulent transactions may trigger prosecution under Section 132 of the CGST Act. While prosecution is typically reserved for high-risk scenarios, authorities may initiate criminal proceedings where revenue loss is substantial or intent to evade tax is evident.

Legal action may involve penalties, recovery proceedings, and prosecution depending on the magnitude of non-compliance and intent assessment by authorities.

GST Prosecution Rule:

Prosecution may occur when non-registration involves deliberate tax evasion, fraudulent transactions, or suppression of turnover causing revenue loss.

| Violation Type | Legal Action | Severity |

|---|---|---|

| Procedural lapse | Penalty | Low |

| Late registration | Penalty + interest | Medium |

| Suppression of turnover | Demand order | High |

| Fraudulent evasion | Prosecution | Very High |

What Common Mistakes Increase GST Penalty Risk for Businesses?

Many businesses unintentionally increase penalty exposure due to misunderstanding compliance rules, delayed corrective action, or reliance on informal advice. Recognizing these mistakes helps prevent enforcement escalation.

- Assuming turnover exemption applies universally

- Ignoring compulsory registration rules

- Continuing operations after eligibility threshold

- Delayed response to GST notices

- Failure to maintain transaction records

- Selling through marketplaces without registration

Incorrect Approach

- Delay registration intentionally

- Ignore eligibility rules

- Operate without documentation

- Avoid notice response

Correct Approach

- Evaluate eligibility early

- Apply registration promptly

- Maintain transaction records

- Respond to notices immediately

Businesses unsure about eligibility or facing penalty risk can opt for professional assistance through GST registration service support for compliant and error-free filing to prevent enforcement complications.

Multi-compliance businesses operating in regulated sectors should ensure coordinated registration across frameworks. For example, MSME registration improves financial credibility, FSSAI licensing is mandatory for food businesses, and Google Business Profile setup strengthens digital legitimacy — collectively reducing compliance risk signals during GST scrutiny.

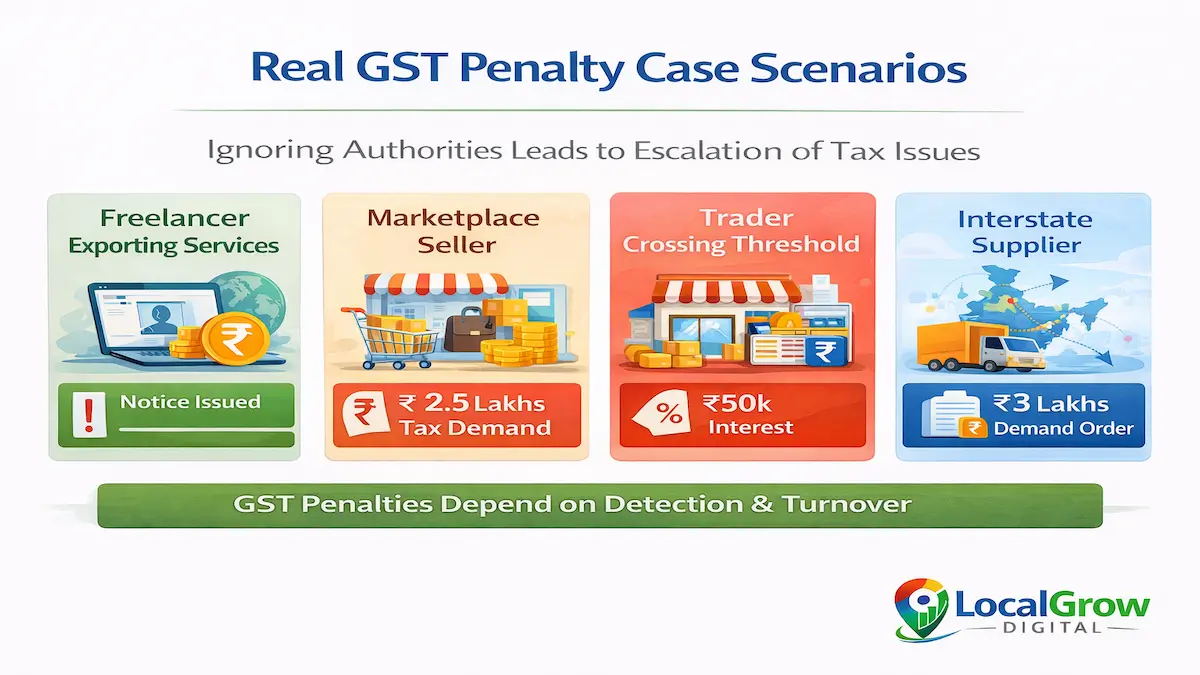

Real Examples: How Businesses Get Penalized for Not Registering GST

Understanding real-world penalty scenarios helps businesses visualize compliance risk beyond theoretical provisions. Many penalties arise not from intentional evasion but from delayed registration due to misunderstanding turnover limits, interstate supply rules, or marketplace compliance requirements.

GST authorities often detect unregistered activity through vendor mismatch, marketplace data integration, or banking analytics, resulting in retrospective tax assessment and penalty imposition. The following scenarios illustrate how enforcement unfolds across different business models.

| Business Type | Violation | Authority Action | Financial Impact |

|---|---|---|---|

| Freelancer exporting services | No GST registration | Notice + tax demand | Medium |

| Online seller marketplace | Compulsory registration ignored | Penalty + recovery | High |

| Trader crossing threshold | Delayed registration | Interest + penalty | Medium |

| Interstate supplier | No registration | Demand order | High |

Can Late GST Registration Reduce Penalty Exposure?

Late GST registration does not eliminate penalty but may reduce enforcement severity when businesses voluntarily regularize compliance before detection. Authorities often differentiate between procedural delay and deliberate tax evasion, influencing penalty magnitude

Businesses proactively applying for registration and paying pending tax liabilities demonstrate compliance intent, which may mitigate risk of prosecution or aggressive recovery proceedings.

Businesses should understand complete registration workflow explained in GST registration process guide before initiating late compliance.

Voluntary compliance before detection significantly reduces enforcement severity and improves officer perception.

— LocalGrow Digital

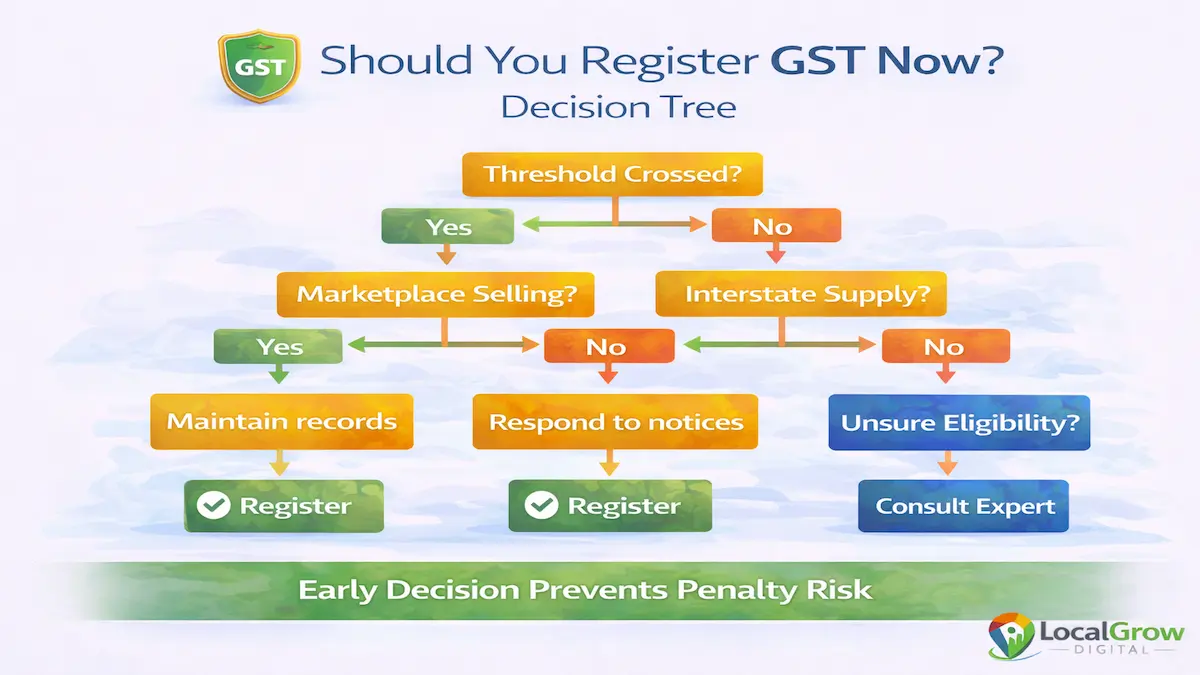

Should You Register GST Immediately After Crossing Eligibility Threshold?

Yes — registering immediately after crossing eligibility threshold is the safest strategy to prevent penalty exposure. Many businesses delay registration expecting future regularization, but retrospective tax assessment and interest accumulation often make delayed compliance financially burdensome.

Timely registration ensures input tax credit eligibility, vendor compliance acceptance, and avoidance of retrospective tax liability that may otherwise disrupt business cash flow.

Delayed Registration Consequences

- Retrospective tax liability

- Interest accumulation

- Penalty imposition

- Vendor mismatch notices

- Higher audit risk

Immediate Registration Benefits

- Compliance protection

- ITC eligibility

- Vendor credibility

- Lower penalty risk

- Financial transparency

Delayed registration exposes businesses to retrospective tax liability and cumulative interest. Expert evaluation ensures accurate compliance decision.

GST Registration Decision Checklist:

• Crossed turnover threshold

• Interstate supply exists

• Selling via marketplace

• Exporting services

• Seeking business credibility

DIY vs Expert GST Registration: Which Reduces Penalty Risk?

While GST portal allows self-registration, incorrect classification, documentation errors, or failure to respond to notices significantly increases rejection and penalty risk. Expert-assisted registration ensures accurate eligibility verification, documentation validation, and professional handling of officer queries.

| Factor | DIY Registration | Expert Assisted |

|---|---|---|

| Eligibility evaluation | Uncertain | Structured |

| Document accuracy | Moderate risk | Verified |

| Notice response | Confusing | Professional |

| Rejection probability | Higher | Lower |

| Long-term compliance | Limited | Strong |

What Financial Risks Increase When Businesses Ignore GST Registration?

Ignoring GST registration creates cumulative financial risk involving tax liability, interest, penalty, and operational disruption. Businesses may also face vendor rejection, inability to claim input tax credit, and difficulty securing loans or marketplace approvals due to compliance gaps.

- Retrospective tax payment obligation

- Interest on unpaid tax

- Penalty imposition

- Vendor compliance rejection

- Marketplace selling restrictions

- Increased audit probability

Can GST Non-Registration Affect Business Loans, Funding, or Partnerships?

Yes — GST compliance is increasingly used as a credibility indicator by financial institutions, investors, and vendors. Non-registered businesses may face challenges securing working capital loans, vendor partnerships, or marketplace onboarding due to perceived compliance risk.

Banks and NBFCs often review GST filing history, turnover declaration, and compliance records during credit evaluation, making delayed registration a potential barrier to business growth opportunities.

Businesses seeking immediate compliance and penalty risk reduction can opt for GST registration assistance service for structured and accurate filing to ensure smooth approval and avoid enforcement complications.

Integrated compliance strengthens business legitimacy. MSME registration improves financial credibility, FSSAI licensing ensures sector-specific compliance for food businesses, and Google Business Profile setup enhances digital authenticity — collectively reinforcing trust signals that reduce compliance scrutiny during GST verification.

Decision Guide: Should You Apply GST Now or Wait?

Businesses often delay GST registration due to uncertainty about eligibility or fear of compliance burden. However, waiting increases cumulative penalty exposure and financial liability, especially when taxable activity already exists.

✔ Register immediately if threshold crossed

✔ Register immediately if interstate supply exists

✔ Register immediately if selling on marketplace

✔ Consider voluntary registration for credibility

✔ Seek expert help if unsure

GST registration is not just a compliance obligation — it is a strategic safeguard against financial and operational risk.

— LocalGrow Digital

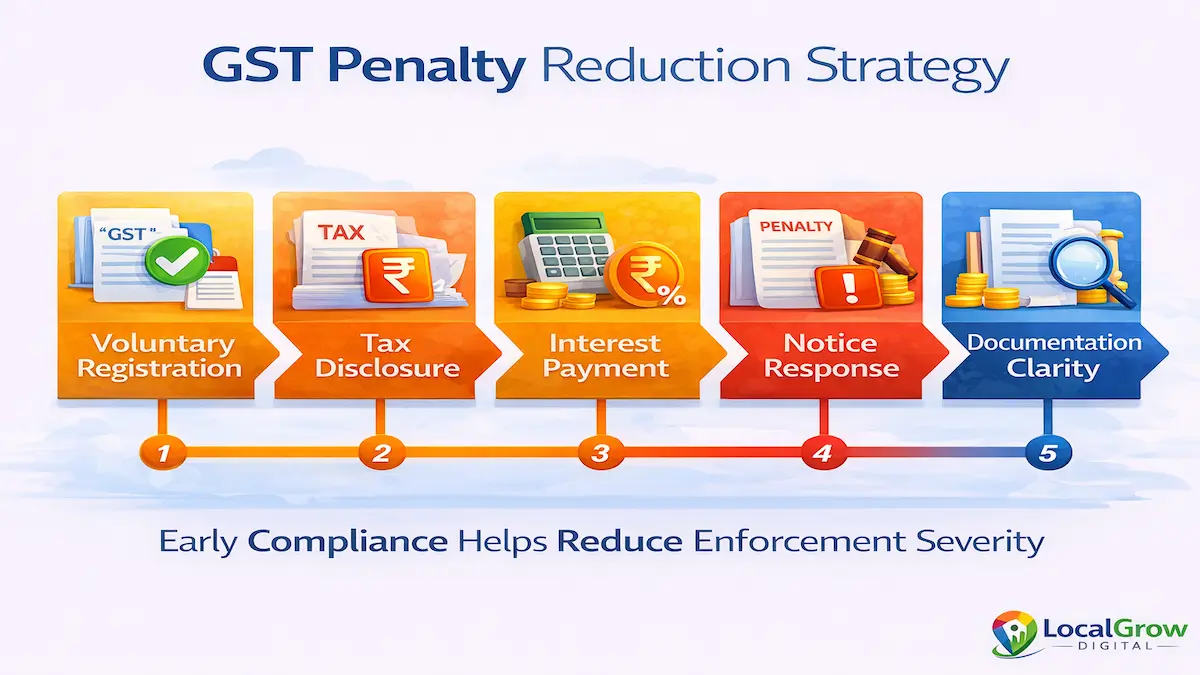

Can GST Penalty Be Reduced After Late Registration?

Yes — GST penalty can be reduced in certain situations when businesses voluntarily register before detection, cooperate with authorities, and clear pending tax liability promptly. Authorities often differentiate between procedural delays and deliberate tax evasion, influencing penalty severity.

GST penalty reduction depends on:

- Voluntary compliance before detection

- Accurate disclosure of turnover

- Prompt payment of tax and interest

- Timely response to notices

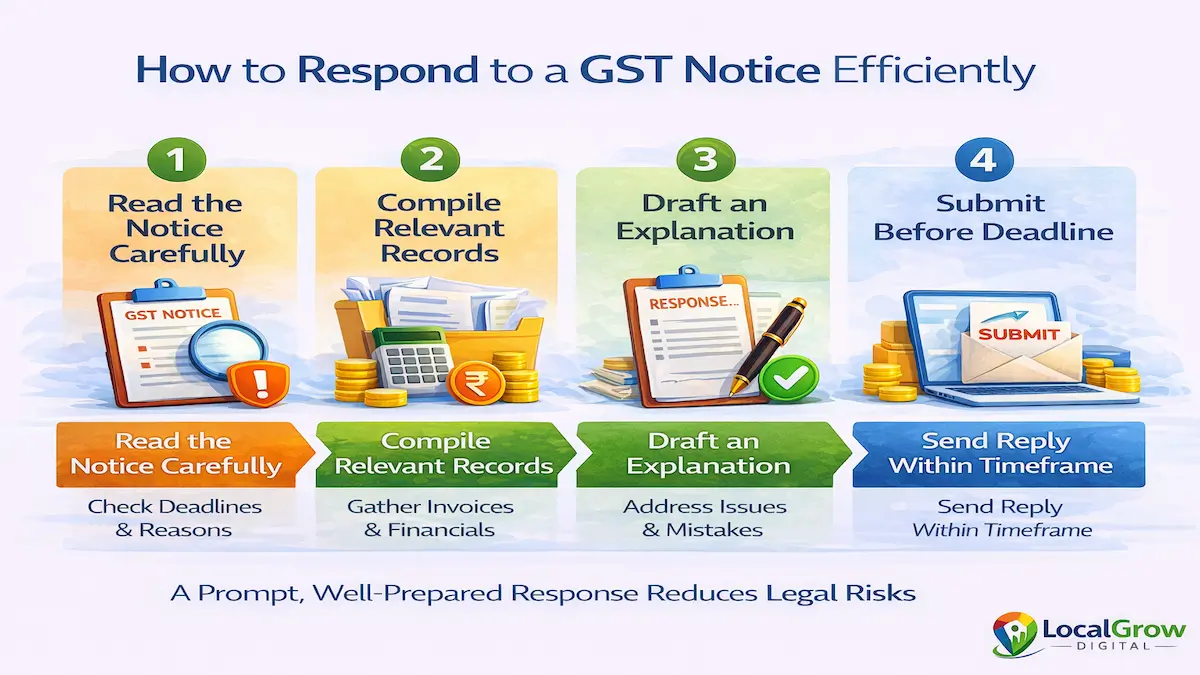

What Should You Do Immediately After Receiving GST Non-Registration Notice?

Receiving a GST notice for non-registration should trigger immediate compliance action rather than panic. Businesses must carefully review notice details, evaluate tax liability, and initiate registration to minimize penalty escalation.

✔ Review notice type and timeline

✔ Calculate tax exposure

✔ Apply GST registration immediately

✔ Respond to notice with documentation

✔ Pay pending tax and interest

Timely response to GST notices significantly reduces penalty escalation and recovery enforcement.

— LocalGrow Digital

Avoid GST penalty escalation by initiating compliance immediately.

How Late GST Registration Helps Reduce Legal Risk

Late registration demonstrates compliance intent and may prevent aggressive enforcement measures such as prosecution or account attachment. Authorities often prioritize revenue recovery over punitive action when businesses voluntarily regularize compliance.

| Action | Impact on Penalty |

|---|---|

| Voluntary registration | Penalty mitigation |

| Prompt tax payment | Interest reduction |

| Notice response | Recovery delay prevention |

| Documentation clarity | Faster approval |

If applications face procedural issues during late compliance, reviewing GST registration rejected in India and corrective measures helps prevent repeated filing errors.

GST Penalty Recovery Timeline After Detection

- Notice issued within few weeks of detection

- Demand order after assessment

- Recovery proceedings if unpaid

- Attachment or enforcement in severe cases

Can Professional Assistance Help Reduce GST Penalty Exposure?

Yes — professional assistance improves documentation accuracy, eligibility evaluation, and notice response strategy, significantly reducing penalty exposure and compliance friction.

Without Expert Help

- Confusing notice interpretation

- Incorrect tax calculation

- Delay in response

With Expert Help

- Structured compliance strategy

- Accurate tax assessment

- Professional officer communication

Businesses facing penalty notices can opt for professional GST registration and compliance assistance to ensure accurate filing, penalty mitigation, and smooth approval.

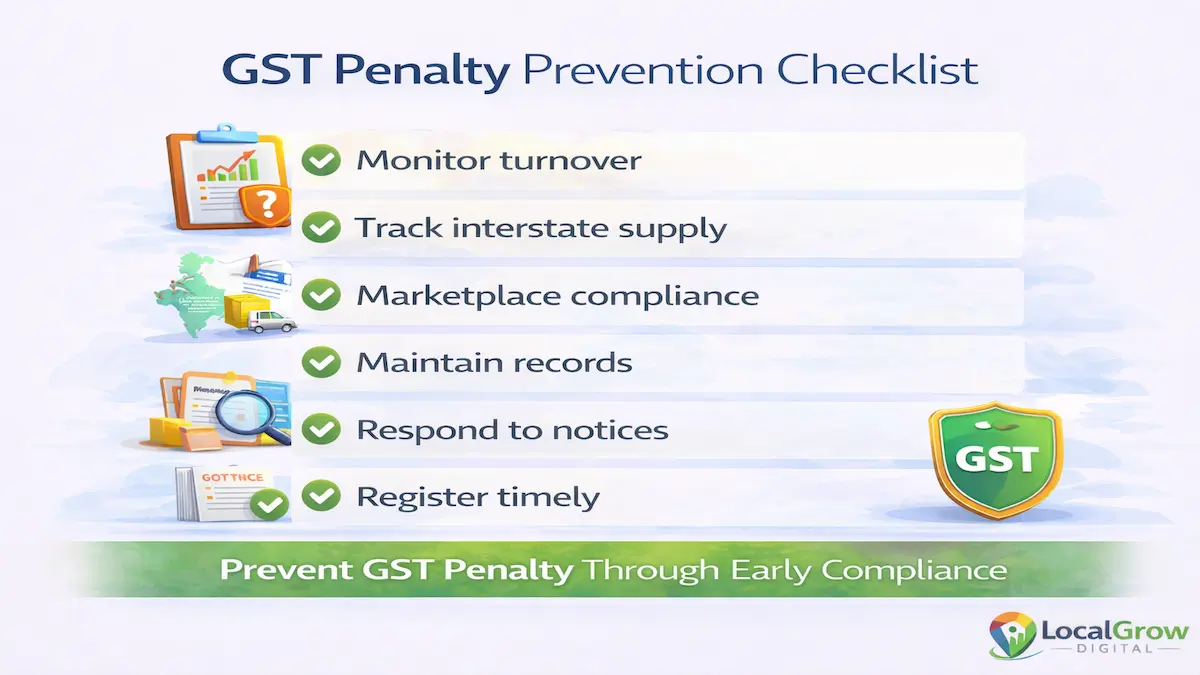

How to Prevent GST Penalty in Future? Practical Compliance Checklist

✔ Monitor turnover regularly

✔ Track interstate supply

✔ Evaluate marketplace compliance

✔ Maintain transaction records

✔ Respond to GST notices promptly

✔ File returns on time

Preventive compliance is always cheaper than penalty recovery.

— LocalGrow Digital

What Common Mistakes Increase GST Penalty Risk After Eligibility?

Many businesses face GST penalties not due to deliberate evasion but because of avoidable compliance mistakes. These mistakes often arise from misunderstanding compulsory registration rules, ignoring digital transaction trails, or delaying corrective action despite receiving eligibility signals.

Authorities evaluate compliance behavior patterns when assessing penalty severity. Businesses that repeatedly ignore eligibility thresholds, fail to respond to notices, or continue interstate supply without registration may face escalated enforcement measures.

- Misinterpreting turnover exemption rules

- Ignoring compulsory registration categories

- Continuing interstate supply without registration

- Selling on marketplaces assuming exemption

- Delayed response to GST notices

- Poor transaction documentation

- Failure to track vendor mismatch alerts

Penalty Risk Rule:

GST penalty risk increases significantly when businesses continue taxable activity after becoming aware of eligibility or receiving compliance notice.

Most GST penalties arise from delayed compliance decisions rather than intentional evasion.

— LocalGrow Digital

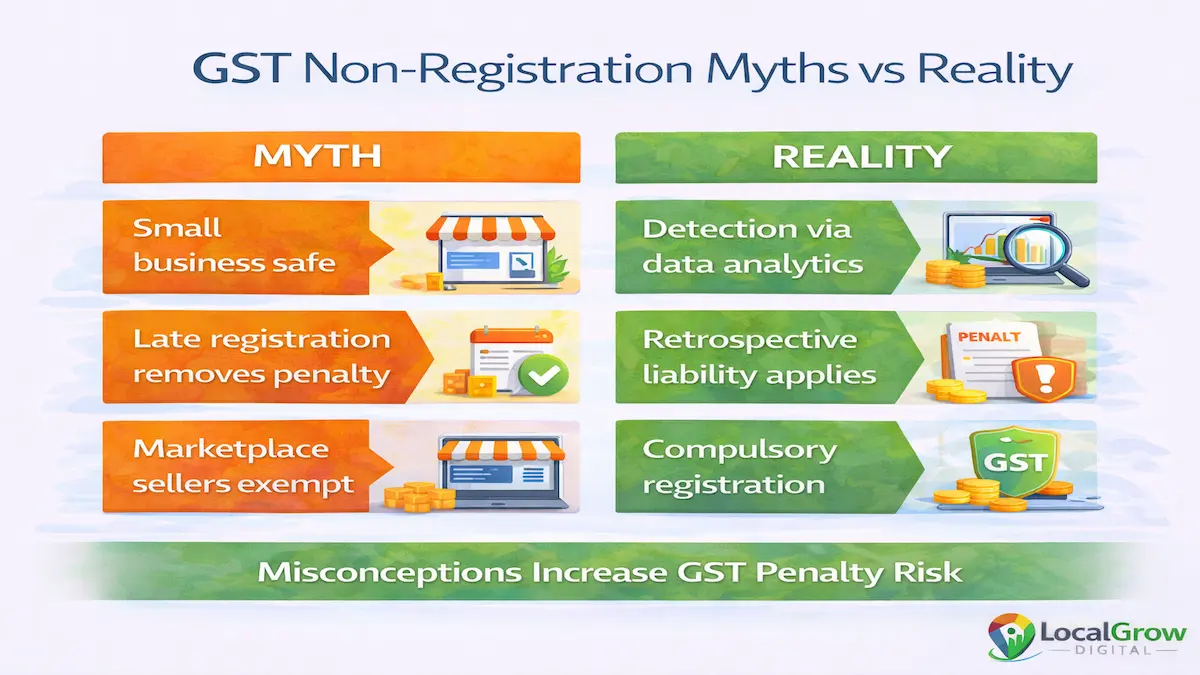

GST Non-Registration Myths vs Reality: What Businesses Often Get Wrong

Misconceptions about GST registration remain one of the primary reasons businesses delay compliance and subsequently face penalty exposure. Understanding these myths helps businesses avoid costly mistakes and align with legal requirements proactively.

| Myth | Reality |

|---|---|

| GST required only after high turnover | Compulsory categories override threshold |

| Small freelancers are exempt | Interstate services may require registration |

| Marketplace sellers can delay GST | E-commerce requires compulsory registration |

| Authorities cannot detect small businesses | Data analytics detect digital transactions |

| Late registration removes penalty | Retrospective liability still applies |

What Hidden Financial Risks Do Businesses Ignore When Delaying GST Registration?

Businesses often focus only on immediate penalty amounts while ignoring hidden financial risks such as cumulative interest liability, input tax credit loss, vendor compliance rejection, and audit-triggered operational disruption. These indirect consequences may significantly exceed statutory penalty amounts.

- Loss of input tax credit eligibility

- Vendor relationship disruption

- Marketplace selling restrictions

- Increased audit probability

- Financing and loan approval challenges

- Reputation and credibility risk

| Risk Type | Direct Impact | Indirect Impact |

|---|---|---|

| Tax liability | Immediate payment | Cash flow strain |

| Interest | Financial cost | Profit margin reduction |

| Penalty | Compliance cost | Working capital pressure |

| Vendor mismatch | Notice issuance | Relationship disruption |

| Audit risk | Investigation | Operational stress |

Why Some Businesses Continue Operating Without GST Despite Penalty Risk

Behavioral and psychological factors often influence delayed GST registration decisions. Many businesses underestimate detection probability, assume turnover exemption applies universally, or prioritize short-term operational convenience over long-term compliance stability.

Understanding these behavioral drivers helps businesses make rational compliance decisions and avoid costly enforcement consequences.

Common Assumptions

- Detection unlikely

- Turnover below threshold

- Compliance burden high

- Penalty manageable

Reality

- Detection probability rising

- Compulsory registration rules apply

- Compliance simplified via experts

- Penalty cumulative and unpredictable

Advanced Risk Matrix: When GST Non-Registration Becomes a Serious Compliance Threat

GST non-registration transitions from procedural lapse to serious compliance threat when specific risk triggers accumulate. Authorities assess risk based on turnover scale, digital transaction visibility, interstate activity, and vendor compliance mismatch patterns.

| Trigger | Authority Interpretation | Severity |

|---|---|---|

| Marketplace sales | Interstate taxable supply | High |

| Export services | Compulsory registration | Medium |

| Vendor ITC mismatch | Hidden taxable activity | High |

| AIS turnover mismatch | Undeclared income | Medium |

| Repeated notice ignoring | Intent assessment | Very High |

Businesses evaluating eligibility scenarios should refer to GST turnover limit in India registration rules to prevent threshold misinterpretation.

How to Avoid GST Penalty Using Preventive Compliance Strategy

Preventive compliance focuses on early eligibility evaluation, transaction monitoring, and timely registration to avoid enforcement escalation. Businesses adopting proactive compliance approach significantly reduce penalty exposure and audit probability.

- Monitor turnover monthly

- Track interstate transactions

- Evaluate marketplace selling rules

- Maintain invoice documentation

- Respond to notices immediately

- Seek expert advice when uncertain

Prevent penalty risk through early compliance evaluation.

Frequently Asked Questions About GST Non-Registration Penalty in India

Businesses frequently search for clarity on GST penalty exposure, detection risk, compliance strategy, and legal implications when registration is delayed. The following expert-level FAQs address real search queries, practical scenarios, and compliance concerns in detail to help businesses understand risks and take corrective action confidently.

Is GST penalty automatically applied if I don’t register on time?

GST penalty is not automatically imposed the moment eligibility threshold is crossed, but it becomes applicable once authorities determine that taxable activity occurred without mandatory registration. The enforcement process typically begins with detection, followed by notice issuance, retrospective tax assessment, and penalty imposition under Section 122 of the CGST Act.

Penalty severity depends on factors such as turnover during non-registration period, intent assessment, tax liability amount, and compliance behavior after detection. Businesses voluntarily registering before detection often face reduced enforcement severity compared to cases where authorities initiate investigation.

Ignoring eligibility signals significantly increases penalty probability because retrospective tax liability combined with interest accumulation forms the basis for enforcement action.

How much penalty do I have to pay if I fail to register GST?

Under GST law, failure to obtain registration when legally required attracts a penalty of ₹10,000 or the tax amount due, whichever is higher. However, the total financial exposure extends beyond this statutory penalty and may include retrospective tax liability, interest on unpaid tax, and potential recovery proceedings.

Businesses often underestimate cumulative exposure because interest under Section 50 accrues daily until tax is paid, increasing financial burden significantly. In cases involving deliberate evasion or suppression of turnover, penalty may escalate up to 100% of tax liability along with prosecution risk.

Therefore, actual financial exposure depends on duration of non-registration, turnover scale, and enforcement outcome.

Can GST department detect small businesses without registration?

Yes — GST authorities increasingly detect unregistered businesses through data analytics, vendor mismatch, banking transaction trails, marketplace reporting, and AIS income analysis. Even small businesses generate digital compliance signals that may trigger scrutiny when inconsistencies appear across tax and financial data systems.

Marketplace sellers, freelancers with interstate clients, and businesses issuing invoices to registered vendors face higher detection probability due to integrated compliance reporting frameworks. Detection does not always require physical inspection; automated analytics often identify taxable activity requiring registration.

As digital compliance infrastructure strengthens, detection probability continues rising even for small and early-stage businesses.

Will late GST registration remove penalty risk?

Late GST registration does not eliminate penalty risk but may reduce enforcement severity when businesses voluntarily regularize compliance before detection. Authorities often distinguish between procedural delay and deliberate non-compliance when assessing penalty magnitude.

Voluntary registration combined with prompt tax payment demonstrates compliance intent and may prevent aggressive recovery measures or prosecution. However, retrospective tax liability and interest remain applicable regardless of voluntary action.

Therefore, late registration should be viewed as a risk-mitigation strategy rather than penalty elimination mechanism.

What happens if I ignore GST notice for non-registration?

Ignoring GST notices significantly increases enforcement severity and may lead to demand orders, recovery proceedings, bank account attachment, or prosecution in severe cases. Notices serve as procedural opportunities for businesses to explain compliance status and initiate corrective action.

Failure to respond within prescribed timeline often results in ex-parte assessment, meaning authorities determine tax liability without taxpayer representation. This may lead to higher penalty exposure due to absence of mitigating explanations or documentation.

Timely response combined with registration application and tax payment remains the most effective strategy to prevent escalation.

Is GST mandatory for freelancers even with low income?

GST registration for freelancers depends on turnover threshold and nature of services provided. Freelancers offering interstate or export services often fall under compulsory registration provisions regardless of turnover, making non-registration a potential compliance violation.

Authorities assess client location, transaction pattern, and banking trail when evaluating freelancer registration obligations. Freelancers mistakenly assuming turnover exemption applies universally may face retrospective tax liability and penalty once authorities detect compulsory registration conditions.

Understanding service classification and transaction geography is critical to evaluating registration requirement accurately.

Can online sellers operate without GST registration?

Online sellers operating through marketplaces generally require GST registration regardless of turnover due to compulsory registration provisions. Marketplaces report seller transaction data through TCS mechanisms, enabling authorities to detect non-registered sellers efficiently.

Operating without GST in such scenarios may lead to penalty, interest liability, and marketplace selling restrictions. Even sellers with modest turnover may face enforcement due to data transparency within marketplace compliance frameworks.

Therefore, online sellers should prioritize registration before commencing marketplace operations.

Can GST non-registration lead to legal prosecution?

Yes — prosecution may occur in severe cases involving deliberate tax evasion, suppression of turnover, or fraudulent transactions causing revenue loss. While prosecution is typically reserved for high-risk scenarios, authorities may initiate criminal proceedings when intent to evade tax is established.

Legal action may involve penalty, recovery proceedings, and prosecution depending on violation severity. Businesses demonstrating voluntary compliance and cooperation generally avoid prosecution risk.

Understanding enforcement thresholds helps businesses prioritize timely compliance.

How can I reduce GST penalty after late registration?

Penalty reduction depends on voluntary compliance behavior, prompt tax payment, accurate disclosure of turnover, and timely response to notices. Authorities often consider mitigating factors when assessing enforcement severity, particularly when businesses proactively initiate compliance before detection.

Seeking professional guidance, maintaining documentation transparency, and cooperating with authorities significantly improves probability of penalty mitigation. However, retrospective tax and interest remain applicable.

Penalty reduction strategies should focus on compliance regularization rather than avoidance.

Does GST non-registration affect business credibility and loans?

Yes — GST compliance increasingly serves as a credibility indicator for financial institutions, investors, and vendors. Non-registered businesses may face challenges securing loans, vendor partnerships, or marketplace onboarding due to perceived compliance risk.

Banks frequently review GST filing history and turnover declarations during credit evaluation, making delayed registration a barrier to financial growth opportunities. Compliance improves transparency, strengthens financial credibility, and supports business expansion initiatives.

What happens if I cross GST threshold but delay registration for few months?

Crossing GST threshold without registration triggers retrospective tax liability from the date eligibility began. Even if registration is obtained later, authorities may assess tax for the period of non-registration along with interest and penalty depending on compliance behavior.

Delayed registration also affects input tax credit eligibility and may create vendor mismatch notices if transactions occurred with registered businesses. Authorities evaluate turnover records, bank transactions, and marketplace data when assessing retrospective liability.

Voluntary registration shortly after threshold crossing reduces enforcement severity but does not eliminate liability for past taxable activity.

Can GST penalty be avoided if I stop business after crossing threshold?

Stopping business does not automatically eliminate GST liability if taxable activity occurred after eligibility threshold was crossed. Authorities may still assess tax and penalty for the period during which registration was required but not obtained.

The critical factor is whether taxable supplies were made during the non-registration period. If business activity continued without registration, retrospective tax and interest may apply regardless of later closure.

Businesses should consider voluntary registration and compliance regularization even when operations cease to prevent future enforcement complications.

What if I didn’t know GST registration was mandatory?

Lack of awareness does not exempt businesses from GST penalty because tax compliance operates under statutory responsibility principles. However, authorities may consider compliance behavior and voluntary corrective action when assessing penalty severity.

Demonstrating prompt registration after awareness, accurate disclosure of turnover, and cooperation during assessment may mitigate enforcement intensity. Nonetheless, retrospective tax and interest remain applicable.

Businesses should regularly evaluate eligibility criteria to avoid compliance gaps caused by misinformation or misunderstanding.

Can GST department check my bank transactions for non-registration?

Yes — authorities may analyze banking transactions through data integration frameworks to identify turnover inconsistencies and potential non-registration cases. Financial transaction visibility across regulatory systems enables detection even without physical inspection.

High-volume digital transactions, repeated business receipts, and mismatch between AIS data and GST registration status may trigger scrutiny. Banking analytics combined with marketplace reporting significantly increases detection probability.

Maintaining transparency and evaluating eligibility early reduces enforcement risk arising from financial data analysis.

Is GST registration required if my clients are from different states?

Providing services or supplying goods across state boundaries often triggers compulsory GST registration regardless of turnover threshold. Interstate supply is treated as taxable activity requiring compliance under GST law.

Freelancers, consultants, and digital service providers working with out-of-state clients frequently fall under compulsory registration provisions even with modest turnover. Ignoring this requirement may result in penalty exposure once authorities detect transaction geography.

Evaluating client location and supply classification is essential to determine registration obligation accurately.

What happens if my vendor asks for GST but I’m not registered?

Vendors may require GST registration to claim input tax credit and maintain compliance records. Supplying goods or services to registered vendors without GST registration may trigger vendor mismatch alerts and compliance notices.

Registered vendors report purchase data, enabling authorities to detect unregistered suppliers involved in taxable transactions. This data mismatch often becomes a detection pathway leading to notice issuance.

Obtaining GST registration ensures vendor compliance compatibility and prevents transaction disruptions.

Can GST penalty apply even if I earn small profits?

GST liability is based on turnover and nature of supply rather than profit margin. Even businesses with modest profitability may face penalty if turnover exceeds eligibility threshold or compulsory registration conditions apply.

Authorities assess gross turnover and taxable supply activity when determining registration obligation. Therefore, profit level does not influence compliance requirement or penalty applicability.

Understanding turnover-based compliance framework helps businesses avoid misconceptions linking GST obligation to profit size.

Will GST registration increase my tax burden significantly?

GST registration does not necessarily increase tax burden because input tax credit allows businesses to offset tax paid on purchases against output liability. Many businesses experience improved tax efficiency after registration due to credit eligibility.

However, compliance obligations such as return filing and record maintenance increase after registration. Businesses should view GST as compliance framework rather than additional tax layer, particularly when credit mechanism applies.

Evaluating transaction structure and input credit availability helps assess actual financial impact of registration.

Can GST non-registration affect marketplace selling accounts?

Yes — marketplaces often require GST registration for sellers due to TCS compliance and interstate transaction nature. Non-registered sellers may face account restrictions, listing limitations, or enforcement action by marketplace compliance teams.

Marketplace transaction data is shared with tax authorities, increasing detection probability for non-registered sellers. Sellers should prioritize registration before scaling marketplace operations to avoid disruption.

Compliance ensures smoother marketplace onboarding and sustained selling capability.

Is voluntary GST registration safer even if threshold not crossed?

Voluntary registration can be beneficial for businesses seeking vendor credibility, input tax credit eligibility, and compliance preparedness. While not mandatory below threshold, voluntary registration reduces risk of accidental non-compliance when turnover fluctuates.

Authorities treat voluntary registrants as fully compliant taxpayers with standard obligations. Businesses anticipating interstate supply, marketplace expansion, or vendor collaboration often choose voluntary registration as preventive compliance strategy.

Evaluating growth trajectory and transaction pattern helps determine suitability of voluntary registration.

How does GST department calculate tax liability for non-registration period?

When a business fails to register despite eligibility, authorities calculate tax liability retrospectively from the date registration became mandatory. The calculation includes taxable turnover during the non-registration period, applicable GST rate, and adjustments for eligible input tax credit subject to documentation availability.

Authorities analyze invoices, banking transactions, marketplace reports, AIS data, and vendor mismatch signals to estimate turnover. In absence of complete records, best judgment assessment may be applied, potentially increasing liability exposure.

Interest under Section 50 accrues from the due date of tax payment until settlement, significantly increasing financial impact over time.

Can GST officer conduct audit for non-registration cases?

Yes — authorities may initiate audit or inspection when non-registration is detected and turnover appears substantial. Audit scope typically includes turnover verification, transaction analysis, invoice examination, and bank record review to determine accurate tax liability.

Audit may occur through document scrutiny, on-site inspection, or data-based assessment depending on risk profile. Businesses demonstrating voluntary compliance and accurate documentation often experience smoother audit outcomes compared to cases involving inconsistent records.

Maintaining transparent financial records and responding promptly to notices reduces audit escalation risk.

What legal sections apply when GST registration is not obtained?

Failure to obtain GST registration primarily attracts penalty under Section 122 of the CGST Act. Interest liability arises under Section 50 for delayed tax payment, while severe cases involving deliberate evasion may trigger prosecution provisions under Section 132.

Additionally, Rule 9 governs application verification procedures, and enforcement mechanisms may include demand orders and recovery proceedings. Authorities assess violation severity and intent when determining applicable legal provisions.

Understanding these legal references helps businesses evaluate compliance risk accurately.

Can GST non-registration lead to bank account attachment?

Bank account attachment may occur during recovery proceedings when assessed tax and penalty remain unpaid after demand order issuance. Authorities use attachment as enforcement tool to secure revenue and compel compliance in high-risk or persistent default cases.

Attachment typically follows notice issuance, assessment, and opportunity for representation. Businesses proactively responding to notices and settling liability generally avoid such enforcement escalation.

Timely compliance remains the most effective prevention strategy.

What is best judgment assessment in GST non-registration cases?

Best judgment assessment occurs when authorities estimate tax liability based on available data due to incomplete records or non-cooperation by taxpayer. This method relies on banking transactions, marketplace turnover, vendor reports, and industry benchmarks to approximate taxable turnover.

Best judgment assessment may lead to higher liability due to conservative estimation assumptions. Businesses maintaining accurate documentation and cooperating with authorities reduce reliance on this method and ensure fair assessment.

Understanding this mechanism highlights importance of record maintenance even during non-registration period.

Can GST registration be backdated to reduce penalty?

GST registration itself is not backdated; however, tax liability is calculated retrospectively from the date eligibility arose. This means businesses must pay tax for past taxable activity regardless of registration approval date.

Voluntary registration demonstrates compliance intent but does not eliminate retrospective liability. Authorities evaluate turnover history to determine applicable tax and interest for non-registration period.

Therefore, backdating is not a penalty avoidance mechanism but a liability calculation principle.

What happens if GST liability calculated is incorrect?

Businesses have the right to respond to assessment notices and provide supporting documentation to correct liability calculation errors. Authorities allow representation during adjudication process, enabling taxpayers to submit invoices, bank records, and transaction evidence for accurate assessment.

Failure to challenge incorrect calculation may result in demand order based on available data. Seeking professional assistance helps ensure accurate representation and liability determination.

Timely response remains critical to prevent escalation.

Can GST penalty be waived by authorities?

Penalty waiver is not automatic but may occur in specific circumstances where authorities consider mitigating factors such as voluntary compliance, genuine procedural error, or absence of fraudulent intent. Interest liability typically remains non-waivable due to statutory nature.

Authorities exercise discretion based on compliance behavior and representation submitted during adjudication. Businesses demonstrating transparency and cooperation improve probability of penalty reduction or partial waiver.

However, reliance on waiver should not replace proactive compliance.

How does GST non-registration affect input tax credit eligibility?

Input tax credit cannot be claimed for purchases made during the non-registration period because credit eligibility arises only after obtaining GST registration and fulfilling documentation requirements. This leads to hidden financial cost beyond statutory penalty.

Businesses may face higher effective tax burden due to inability to offset input tax during non-registration period. Retrospective tax liability combined with ITC loss significantly increases financial exposure.

Early registration ensures credit optimization and financial efficiency.

Can GST non-registration trigger future audit risk even after compliance?

Yes — non-registration history may increase audit probability due to perceived compliance risk. Authorities may scrutinize post-registration filings, turnover declarations, and return accuracy to ensure consistency with historical data.

Businesses maintaining accurate documentation and demonstrating consistent compliance after registration generally mitigate long-term audit risk. However, enforcement systems may flag past non-registration as risk indicator for periodic review.

Proactive compliance strategy reduces long-term enforcement friction.

Should I apply GST immediately even if I am unsure about eligibility?

When eligibility is uncertain, the safest approach is to conduct professional evaluation rather than delay registration. Many businesses assume turnover exemption applies universally, but compulsory registration categories such as interstate supply, export services, or marketplace selling override threshold limits.

Applying GST after eligibility confirmation prevents retrospective tax liability and cumulative interest exposure. Expert assessment helps avoid unnecessary registration while ensuring compliance when mandatory conditions exist.

Therefore, proactive eligibility evaluation represents the most risk-balanced strategy.

Is GST registration difficult and time-consuming?

GST registration itself is a structured portal process and typically not complex when documentation and classification are accurate. Most delays occur due to incorrect document upload, Aadhaar authentication failure, or officer clarification notices triggered by incomplete information.

Expert-assisted registration reduces procedural errors and ensures faster approval. Businesses prepared with proper documentation often receive GSTIN within a few working days without verification delays.

Perceived complexity should not discourage compliance because structured filing simplifies approval significantly.

Can expert assistance really reduce GST penalty risk?

Yes — expert assistance improves eligibility evaluation, documentation accuracy, notice response strategy, and classification correctness, collectively reducing penalty exposure. Professionals understand officer verification patterns and compliance requirements, enabling proactive risk mitigation.

Businesses handling registration independently may overlook compulsory registration triggers or fail to respond effectively to notices, increasing enforcement risk. Professional guidance ensures compliance readiness and prevents procedural mistakes leading to penalty escalation.

Expert support should be viewed as compliance investment rather than cost.

What is the safest strategy to avoid GST penalty completely?

The safest strategy involves early eligibility evaluation, timely registration, accurate turnover disclosure, and consistent compliance behavior after approval. Monitoring interstate transactions, marketplace activity, and vendor mismatch signals helps detect eligibility triggers before enforcement.

Maintaining documentation transparency and responding promptly to GST notices further reduces penalty exposure. Preventive compliance is significantly more cost-effective than penalty recovery after detection.

Businesses adopting proactive compliance mindset rarely face enforcement complications.

Can I start GST registration now even if penalty risk already exists?

Yes — initiating GST registration immediately remains beneficial even when penalty risk exists. Voluntary compliance demonstrates intent and may reduce enforcement severity while preventing additional liability accumulation.

Authorities typically prioritize revenue recovery over punitive action when businesses proactively regularize compliance. Prompt registration combined with tax settlement improves officer perception and reduces escalation risk.

Delaying further only increases cumulative interest and enforcement probability.

What is the minimum penalty for not registering GST in India?

Penalty under Section 122 is ₹10,000 or the tax amount due, whichever is higher. However, real exposure often includes retrospective tax liability and interest under Section 50, making total financial impact substantially higher. The minimum penalty applies primarily in procedural violation scenarios without evidence of deliberate evasion.

How long can a business operate without GST before penalty applies?

Penalty applicability is linked to eligibility date rather than duration. The moment a business becomes liable for registration and continues taxable activity without compliance, retrospective liability begins. Authorities may detect violation months or years later, leading to cumulative interest and penalty exposure.

Can GST penalty be imposed even without issuing invoices?

Yes. Authorities evaluate actual taxable supply rather than invoice issuance. Banking transactions, marketplace sales, and digital payment trails may establish turnover even without formal invoices, enabling penalty imposition based on detected activity.

Does GST non-registration affect ITC eligibility for buyers?

Yes. Buyers cannot claim input tax credit on purchases from unregistered suppliers. This may lead to vendor rejection, transaction disputes, and compliance notices, indirectly affecting business relationships and growth opportunities.

Can GST registration after notice reduce interest liability?

Interest liability is statutory and continues until tax payment. While registration demonstrates compliance intent and may mitigate penalty severity, interest remains payable for delayed tax settlement.

What documents help defend GST penalty cases?

Supporting documents include invoices, bank statements, transaction records, contracts, marketplace reports, and correspondence explaining eligibility interpretation. Accurate documentation enables representation during adjudication and reduces risk of best judgment assessment.

Can GST non-registration affect future compliance rating?

Yes. Non-registration history may increase scrutiny, audit probability, and compliance risk perception. Authorities monitor behavioral patterns when evaluating taxpayers, making proactive compliance important for long-term credibility.

Is GST registration mandatory for service providers below threshold with interstate clients?

Often yes. Interstate supply of services may trigger compulsory registration provisions even below threshold, exposing service providers to penalty if compliance is ignored.

Can GST department reopen past years for non-registration cases?

Authorities may assess past taxable activity once non-registration is detected, subject to statutory limitation periods. Historical turnover data and transaction records may be examined during enforcement.

What is the fastest way to resolve GST non-registration penalty risk?

The fastest approach involves voluntary registration, tax liability calculation, prompt payment, and notice response. Professional assistance ensures structured compliance and reduces enforcement escalation.

Compliance delay compounds financial risk, while timely registration protects long-term business stability.

— LocalGrow Digital

Avoid GST Penalty and Secure Business Compliance with Expert Assistance

GST non-registration penalty is not merely a financial burden but a compliance risk capable of affecting business credibility, vendor relationships, and growth opportunities. Proactive registration ensures tax transparency, credit eligibility, and regulatory stability while preventing enforcement escalation.

Businesses uncertain about eligibility, facing penalty exposure, or receiving GST notices can benefit from structured compliance support to ensure accurate filing and smooth approval without procedural delays.

Start compliance today and prevent penalty escalation with expert guidance.

GST Non-Registration Penalty — Key Compliance Takeaways

✔ GST registration mandatory once eligibility arises

✔ Penalty includes tax liability, interest, and enforcement risk

✔ Detection probability increasing through data analytics

✔ Voluntary compliance reduces enforcement severity

✔ Preventive registration is safest strategy

✔ Expert assistance improves approval and reduces risk